Hi, we're here to talk about how to calculate IRS penalties if you're late on your tax return. The IRS will levy penalties and interest for late filings. They have a penalty for failure to file, which is five percent per month on the amount that you owe. Additionally, they have a penalty for failure to pay, which is one-half percent per month on the amount that you owe. Moreover, there are interests on the amount that you owe, calculated at the federal short-term rate plus three percent per month. All of these penalties begin on the day that the return is due, which is typically April fifteenth, and will continue until the amount is paid in full. As you can see, if you do the calculations, you'll note that many times the penalties and interest will surpass the original amount owed. Therefore, it's in your best interest to take two steps. First, file your return to eliminate a significant portion of the penalty right there. Second, even if you are unable to pay the full amount, make arrangements with the IRS to set up a payment program of some sort. This will help you avoid the accrual of further penalties and interest. Remember, it's crucial to be proactive when dealing with the IRS to minimize the financial consequences of late filings and payments. So, ensure you file your return and communicate with the IRS to establish a manageable payment plan.

Award-winning PDF software

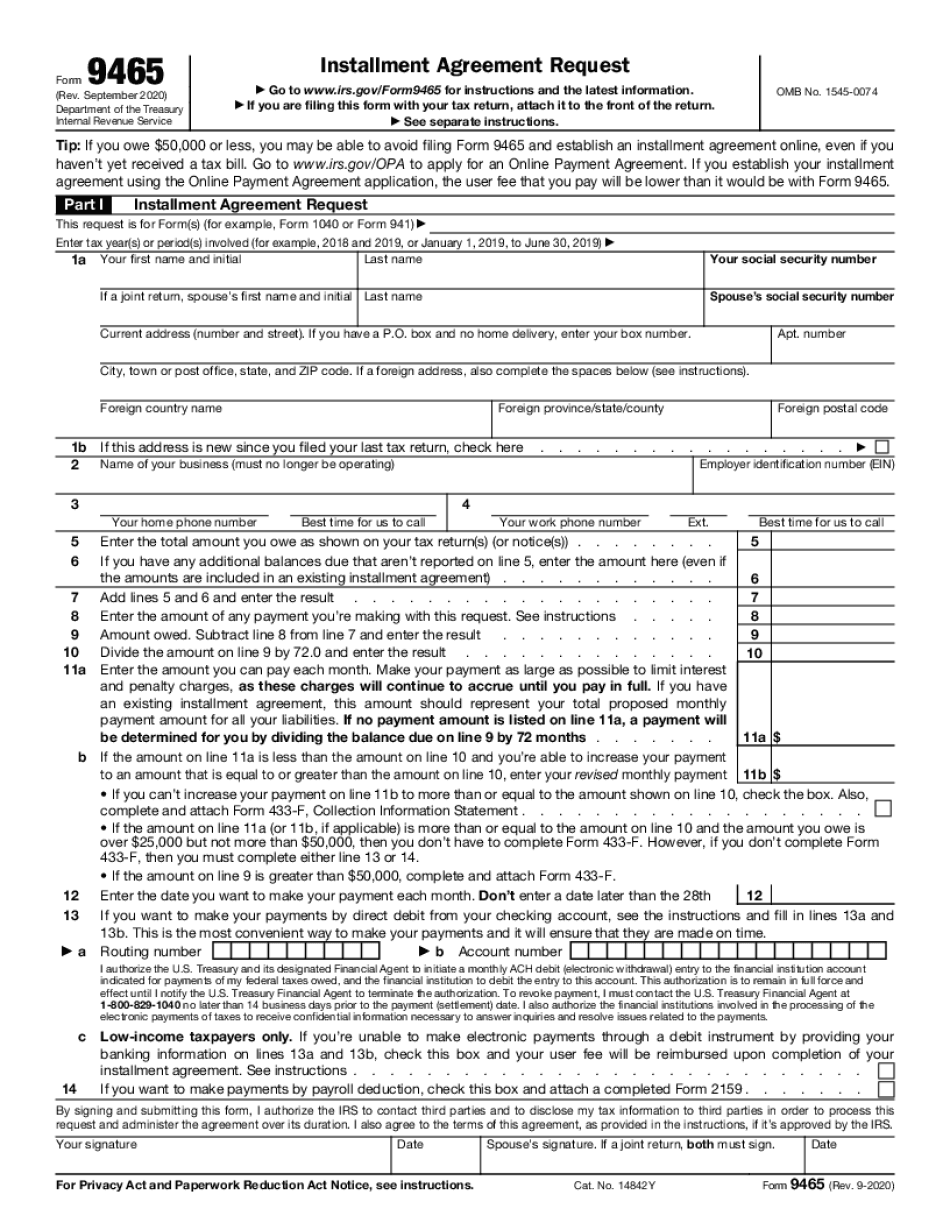

Irs penalty calculator Form: What You Should Know

If you've already filed your return for the current year, you'll need to re-use the previous year's PENALTY form to calculate your penalty amount, as well as your interest amount. The interest rate on penalties, along with the penalty amount, is set, based on the federal rate of 9% for the most recent tax year. The penalty for late processing, whether by you or the IRS, is capped at 20%. The penalty rate for the most recent tax year was 8.9% and the amount of interest that accrues when a tax-filer misses the deadline to file a return for a tax-year is capped at 6%. Learn more. eFile.com PENALTYucator How much do I owe for late filing a tax return? Liable amount for late filing of a return, 2025 IRS Notice 2015-44, Failure to File the Federal Income Tax Return and Estimated Tax Amounts, and IRS Notice 2015-60, Failure to File the Federal Income Tax Return with the Estimated Tax Information, outline the penalties for failure to file a federal tax return. The notice does not provide guidance on how much to pay or avoid penalties. However, the Notice does offer information that will provide taxpayers with key information that can be used to make an informed decision about filing a federal tax return and paying any estimated tax due. Read the IRS Notice 2015-44 and IRS Notice 2015-60. A taxpayer's failure to file or fail to pay any estimated tax is assessed a penalty of the greatest of 50 or 2 percent of the amount of taxes that did or did not satisfy the taxpayer's estimated tax liability or, for an individual who filed a joint return, 100. The penalty also applies to the taxpayer's spouse as well as nonresident aliens and foreign corporations. The penalty assessed is the greatest of 50 or 2 percent of the excess tax in excess of what the taxpayer is required to pay under a single tax system or 100 for nonresident aliens. The IRS has the right to deny a refund because the taxpayer failed to file a tax return or fail to include all the information required by law. For example, in general, income tax returns are tax-exempt for purposes of the Federal Insurance Contributions Act and Federal Unemployment Tax Act (FTA) and the Federal Taxation for Individuals and Foreign Corporations Act (FATWA).

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 9465 online, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 9465 online online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 9465 online by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 9465 online from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Irs penalty calculator